A credit score is a number that shows how good someone is at managing the money they borrow. Think of it as a report card for grown-ups, but instead of grades for math or science, it’s grades for handling money. This score helps banks and other places decide if they should lend you money.

Why is a Good Credit Score Important?

Having a good credit score is important because it makes life easier in many ways. Here’s why:

- Borrowing Money: If you want to buy a car or a house, you might need a loan. A good credit score means banks will trust you more and give you loans at lower interest rates.

- Credit Cards: With a good credit score, you can get better credit cards. These cards often come with rewards like cash back or points you can use for shopping.

- Renting an Apartment: Landlords sometimes check credit scores before letting you rent an apartment. A good score can help you achieve your goals.

- Jobs: Some employers check credit scores when you apply for a job. A good score shows you are responsible.

What Hurts a Credit Score?

Several things can hurt your credit score:

- Late Payments: Paying your bills late can lower your score.

- High Balances: If you use a lot of the money available on your credit cards, your score can go down.

- Applying for Too Much Credit: Asking for many loans or credit cards in a short time can make you look risky to lenders.

- Not Paying Debts: If you don’t pay back money you borrowed, it can seriously harm your score.

How to Repair a Credit Score

If your credit score is low, don’t worry. Here are steps to fix it:

1. Check Your Credit Report

First, you need to know what’s hurting your score. You can get a free copy of your credit report from each of the three major credit bureaus once a year. The credit bureaus are Equifax, Experian, and TransUnion. Check for mistakes like accounts that aren’t yours or wrong balances.

2. Pay Your Bills on Time

One of the easiest ways to improve your score is to pay your bills on time. Set reminders or automatic payments to help you stay on track.

3. Reduce Debt

Try to pay off your credit card balances. Start with the card that has the highest interest rate. Paying off debt shows lenders that you can manage your money well.

4. Avoid Applying for New Credit

Each time you apply for a new credit card or loan, it can hurt your score a little. Only apply when you really need it.

5. Keep Old Accounts Open

The length of your credit history affects your score. If you have old credit cards, keep them open even if you don’t use them often.

6. Use a Mix of Credit Types

Having different types of credit, like a car loan and a credit card, can help your score. But don’t take out loans just to improve your credit mix.

7. Get Help from a Credit Counselor

Sometimes, it helps to get advice from a professional. Credit counselors can help you make a plan to pay off your debt and improve your score.

Tips to Maintain a Good Credit Score

Once your credit score improves, it’s important to keep it in good shape. Here are some tips:

- Stay on Top of Your Bills: Continue to pay your bills on time.

- Use Credit Wisely: Don’t spend more on your credit cards than you can pay off each month.

- Check Your Credit Report Regularly: Make sure there are no mistakes that could hurt your score.

Why It’s Worth the Effort

Repairing and maintaining a good credit score might seem like a lot of work, but it’s worth it. With a good score, you can save money on loans, get better credit cards, and even have more job opportunities. Think of it as an investment in your future.

Real-Life Example of Credit Score

Let’s look at a real-life example to understand better. Emma is a college student who got her first credit card at 18. At first, she didn’t know how to manage it well and ended up with a low credit score. Here’s how she fixed it:

- Emma found out she had some late payments and high balances on her credit report.

- She started using her phone’s calendar to remind her of bill due dates.

- Emma focused on paying off her highest-interest credit card first, then moved to the next one.

- She stopped applying for new credit cards and loans.

- Emma kept her first credit card open, even though she didn’t use it much.

After a year of following these steps, Emma’s credit score improved a lot. She was able to get a better credit card and rent the apartment she wanted.

Credit score repair might seem complicated, but by taking it step by step, anyone can improve their score. It’s all about being responsible with money, paying bills on time, and making smart financial decisions. With patience and effort, you can build a good credit score that will help you in many areas of life.

How Can I Check My Credit Score for Free?

Checking your credit score doesn’t have to cost you anything. You can get your free credit score from many places online. Some websites and apps offer free credit scores as part of their services. Remember, checking your own credit score won’t hurt it. It’s a good idea to check your score regularly to understand your credit health.

What Should a Good Credit Score Be?

A good credit score is like getting an A on your report card. It usually means a score of 700 or higher. A good score shows that you are responsible with money, and banks trust you more. With a good score, you can get loans more easily and at better interest rates.

Is a 900 Credit Score Possible?

A 900 credit score is like getting 100% on a test! While it’s not common, some scoring models might go up to 900. Most credit scores range between 300 and 850. A score above 800 is considered excellent.

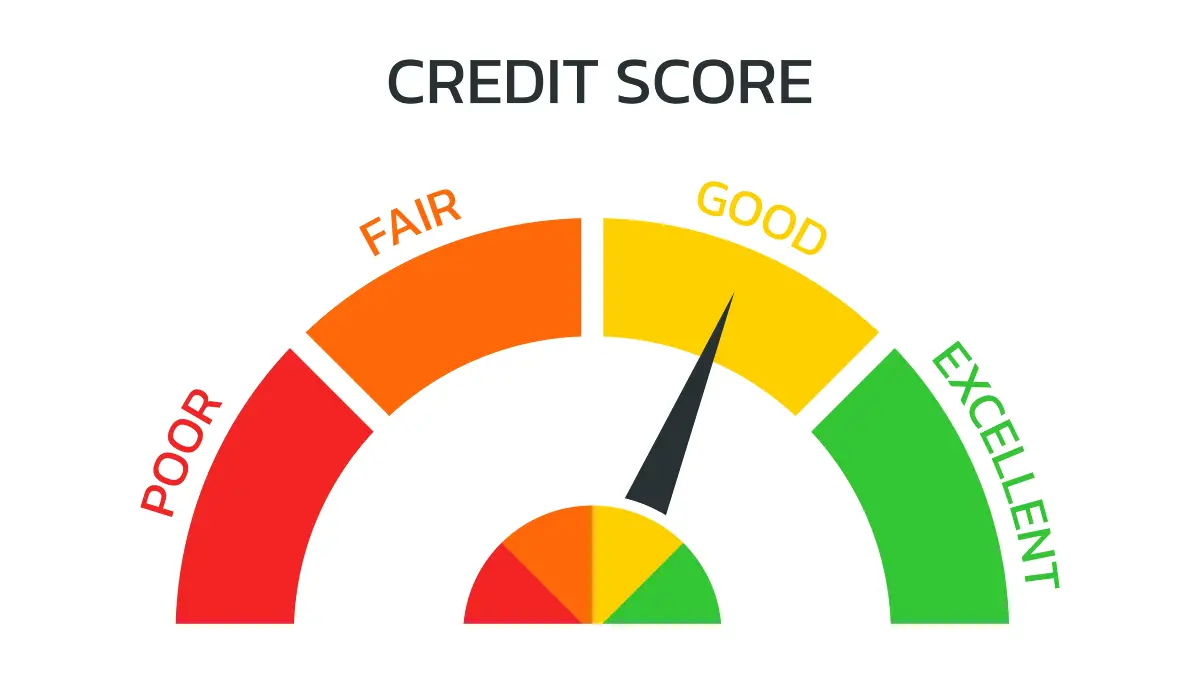

What Are the 5 Levels of Credit Scores?

Credit scores can be grouped into five levels:

- Poor: 300-579

- Fair: 580-669

- Good: 670-739

- Very Good: 740-799

- Excellent: 800-850

Knowing your level can help you understand where you stand and what you can do to improve.

What is a Credit Score?

A credit score is a three-digit number that shows how well you handle borrowing money. It’s based on your credit report, which has information about your credit history. Lenders use this score to decide if they should give you a loan or credit card.

How Lenders Use FICO® Scores

FICO Scores are a type of credit score that many lenders use. They help lenders decide if you’re a good person to lend money to. A higher FICO Score means you’re more likely to get approved for loans and credit cards with good terms.

By understanding these important aspects of credit scores, you can make better financial decisions and work towards a stronger financial future.

Learn About Your Credit Report and How to Get a Copy

Your credit report is a detailed record of your credit history and behavior. It includes information about your credit accounts, payment history, and any public records related to your credit. The three credit bureaus—Equifax, Experian, and TransUnion—compile this information to create your credit report.

How to Get Your Free Credit Report

Under federal law, you are entitled to a free credit report from each of the three credit bureaus once a year. To access your free credit report, you can visit AnnualCreditReport.com. This site is the only website authorized by the federal government to provide free credit reports. Reviewing your credit report regularly is essential to ensure the accuracy of your credit report information and to spot any potential errors or fraudulent activities.

Why Your Credit Report Matters

Your credit report shows lenders and financial institutions your credit health, which helps them determine your creditworthiness. It also plays a crucial role in calculating your credit scores. Regularly checking your credit report can help you maintain a good credit score by ensuring all your credit report information is correct and up-to-date.

By staying informed about your credit report and taking proactive steps to improve your credit behavior, you can work towards achieving a higher credit score and better financial opportunities.

How Often Should You Check Your Credit Score?

Regularly checking your credit score is crucial for maintaining good credit health. It’s recommended to check your credit score at least once a month. This allows you to monitor any changes, catch errors early, and understand how your financial behavior affects your score. Many financial institutions and credit card issuers offer free credit scores as part of their services, making it easy to stay informed.

Why Do You Need a Good Credit Score?

A good credit score opens doors to numerous financial opportunities. It can lead to lower interest rates on loans and credit cards, saving you money over time. Additionally, a high credit score can improve your chances of being approved for a mortgage, auto loan, or personal loan. It also gives you leverage when negotiating credit limits and terms with lenders. In essence, a good credit score reflects responsible credit behavior and can significantly impact your financial well-being.

Understanding the Impact of Credit Utilization on Your Score

Credit utilization is a key factor in determining your credit score. It refers to the ratio of your current credit card balances to your total available credit limits. In simpler terms, it’s how much of your available credit you’re using at any given time. A lower credit utilization ratio indicates that you are using less of your available credit, which can positively impact your credit score. Ideally, you should aim to keep your credit utilization below 30% to maintain a good credit score.

High credit utilization can signal to lenders that you may be over-reliant on credit, which could make you appear risky. This can lead to higher interest rates or even denial of credit applications. To improve your credit utilization, consider paying down existing balances, asking for a credit limit increase, or spreading out your expenses across multiple credit accounts. By managing your credit utilization effectively, you can enhance your credit score and improve your overall financial health.

The Role of Credit Mix in Determining Your Credit Score

Credit mix refers to the variety of credit accounts you have, such as credit cards, mortgages, auto loans, and student loans. Having a diverse credit mix can positively affect your credit score because it demonstrates your ability to manage different types of credit responsibly. Lenders like to see that you can handle a combination of revolving credit (like credit cards) and installment credit (such as loans).

However, it’s important not to take out loans or open new credit accounts solely to improve your credit mix. Instead, focus on using the credit you need and managing it well. By maintaining a balanced mix of credit accounts and making on-time payments, you can contribute positively to your credit score. This, in turn, enhances your creditworthiness and opens up more financial opportunities, such as better loan terms and higher credit limits.

Do I Need to Know My Credit Score?

Yes, knowing your credit score is essential for managing your financial future. It provides insight into your creditworthiness and helps you make informed decisions when applying for loans or credit cards. By understanding your credit score, you can take proactive steps to improve it, ensuring you have access to the best financial products and terms available.

What If I’m Denied Credit or Insurance, or Don’t Get the Terms I Want?

If you’re denied credit or insurance, or if you receive unfavorable terms, it’s important to understand why. Lenders and insurers are required to provide you with an explanation, often referred to as an adverse action notice. This notice will highlight the factors that influenced their decision, such as a low credit score or high credit utilization ratio. Use this information to address any issues and improve your credit standing. You can also request a free credit report to review the details and ensure accuracy.

How Much Does a Credit Check Affect Your Scores?

A credit check, or inquiry, can impact your credit scores, but the effect is usually minimal. There are two types of inquiries: soft and hard. Soft inquiries, such as checking your own credit score or pre-approval offers, do not affect your scores. Hard inquiries, which occur when you apply for a loan or credit card, may lower your score slightly. However, the impact is temporary and typically diminishes over time. To minimize the effect of hard inquiries, avoid applying for multiple credit accounts in a short period.

By understanding these aspects of credit scores and taking proactive steps to manage your credit, you can achieve a higher credit score and enjoy the financial benefits it brings.

Frequently Asked Questions

How can I check my credit score for free?

You can check your credit score for free from various online platforms. Many websites and apps offer free credit scores as part of their services. Remember, checking your own credit score won’t hurt it, and it’s a good idea to check your score regularly to understand your credit health.

What should a good credit score be?

A good credit score is typically 700 or higher. It indicates that you are responsible with money, and banks are more likely to trust you. With a good score, you can obtain loans more easily and at better interest rates.

Is a 900 credit score possible?

While a 900 credit score is not common, some scoring models might go up to 900. Most credit scores range between 300 and 850, with a score above 800 considered excellent.

What are the 5 levels of credit scores?

Credit scores can be grouped into five levels:

- Poor: 300-579

- Fair: 580-669

- Good: 670-739

- Very Good: 740-799

- Excellent: 800-850

Knowing your level can help you understand where you stand and what you can do to improve.

5 Responses